How to calculate gross profit. Definition and formula for calculating gross profit

Gross profit– this is a key criterion for the activity of an enterprise, characterizing its effectiveness. The calculation of this indicator makes it possible to highlight promising directions work of the organization, distribute financial assets into more profitable niches, answer the question: .

What is gross profit?

Maximizing income is the goal of any business enterprise. Gross profit is the amount of money that is received from the sale of a particular product or service minus expenses.

In order for a company to receive it, the goods or services being sold must be in demand. Pricing policy largely depends on the cost of production; production costs are also important. The indicator makes it possible to determine how effectively tangible and intangible assets are used.

Gross profit is the difference between total revenues and expenses. It can be calculated by subtracting the costs of production, purchase, and organizational issues from the proceeds from the sale of products (services). Proceeds are all the money received from the sale. Cost includes all existing costs of producing a product. If the company provides services, the calculation includes all costs associated with their provision.

Gross profit can be determined at any time for any period of time, it all depends on the company’s management accounting, on. As a rule, it is calculated at the end of the month, quarter and year

Calculation formula

To determine gross profit, two indicators are used - revenue and technological cost for the entire volume of production (excluding commercial and administrative costs). There are other types of calculations. Let's look at the main ones.

Calculation of gross profit

Calculation for trading companies

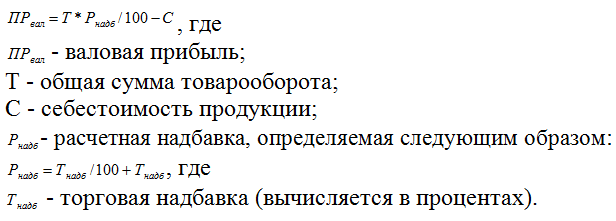

Calculation of goods turnover

This method is used by retail companies if the same markup is set for all products sold by the company. In some cases, it is more convenient to calculate this indicator based on the value of the company’s turnover. Trade turnover is the amount of revenue including value added tax. To do this you need:

You can also apply the following formula:

Balance calculation

Often, for calculations, data is taken from the enterprise’s balance sheet and financial statements. financial activities companies. This method relevant for enterprises operating on . In this case, the calculation algorithm looks like this:

Line 2100 = page 2110 – page 2120, where

- line 2100 – gross profit (indicated in the balance sheet);

- line 2110 – the amount of revenue of the enterprise under study;

- line 2120 – technological cost.

Calculation examples

Example 1 (on balance):

OJSC "Intensive" is engaged in the production and sale of agricultural machinery. Its financial results for last years(according to data on the financial activities of the enterprise):

Calculation of gross profit of OJSC "Intensive":

As can be seen from the calculations, over the year the company increased its income by 40 thousand rubles, so in 2017 it must continue to work according to the chosen strategy, while looking for new ways of development.

Example 2 (for trade turnover):

At the Yagodka grocery store, a markup of 35% is set on all products. For the year, the total revenue amounted to 150,000 rubles (including VAT).

The calculated allowance will be: P(surcharge) = 35%: (100%+35%) = 0.26. In this case, the amount of the realized overlay will be: 0.26 * 150,000 rubles. = 39,000 rubles.

Where is gross profit calculation used?

Gross profit is also determined when drawing up budgets, when distributing monetary assets for the next quarter or year.

note: Gross profit depends on the production process and does not always reflect the real picture of the enterprise’s efficiency. For example, it does not take into account marketing and logistics costs. Therefore, to draw up the final budget, calculating one such indicator will not be enough.

What does gross profit calculation include?

Depending on the field of activity of the enterprise, the cost and income items that are included in the cost and revenue may differ. This should be taken into account when calculating.

The revenue of a manufacturing enterprise depends on:

- specifics and manufacturing technologies of products;

- fixed assets;

- issue of shares, bonds;

- intangible assets;

- sold products or services of other divisions of the company that are included in the balance sheet of the enterprise (vehicle fleet, auxiliary structures).

The cost of such companies includes:

- price of materials, resources, raw materials, fuel;

- staff salaries;

- administrative expenses;

- depreciation;

- overhead costs;

- transportation and logistics costs.

The revenue of companies that sell goods depends on:

- cost of purchased products;

- paid services (after-sales service, delivery);

- company assets (software, securities).

The cost of trading companies consists of the following items:

- price of purchased products;

- delivery costs;

- wage company employees;

- rental of retail and warehouse premises;

- storage of goods, preparatory work;

- marketing.

All of the above expenses and income must be taken into account when calculating economic indicators.

Common mistakes and subtleties when calculating

Often the product is written off as a minus. This means that, according to documents, the products are not in stock, but are still being sold. If there is a surplus of goods or mis-grading, you need to take an inventory of the warehouse and capitalize the surplus. It is important to do this before the products are sold.

Gross profit is often confused with marginal profit. Some sources still identify these concepts today. In fact, the difference is that gross profit is the difference between revenue and variable and fixed expenses. Marginal takes into account only variable costs.

In practice, the company often incurs fixed costs, so gross income is less than marginal income. Fixed expenses include rent, utilities, and depreciation.

Save the article in 2 clicks:

Any commercial company, when making important decisions, is based on profitability indicators. Gross profit is indicated in the balance sheet; it is important for the production sector, as it makes it possible to analyze the technological cost. The indicator is taken into account when planning for 1-3 years, to build a strategy and tactics of action.

In contact with

The activities of any company are aimed at making a profit, which is a qualitative indicator of the feasibility of its activities. Gross profit is characterized by the rational use of all enterprise resources.

Concept of gross income

Profit is the division of the costs of producing products (rendering services) by revenue from their sales.

Gross profit shows the feasibility of the enterprise. This is the ratio of the cost of production to the income from its sale.

When comparing gross profit with net profit, it is important to remember that the former consists not only of production costs, but also of taxes.

Calculation formula

Gross profit can be calculated as follows:

VP = D - (S+Z), where:

- VP - gross profit;

- D - volume of sales of manufactured products (services) in monetary units;

- C - cost of production of products (or services);

- Z - production costs.

To calculate, it is necessary to subtract the cost of products (services) sold from the amount of revenue.

Gross profit formula for financial statements

The indicator “Gross profit” (line 2100) is calculated as follows: “Cost of sales” (line 2120) is subtracted from “Revenue” (line 2110).

The essence of a competent calculation of gross profit is a detailed study of all cost items that are included in the cost of products (services provided). It is necessary to take into account all cost items, especially those not taken into account initially and those that appeared during the sale of products (services).

There is a fairly well-known definition of cost: these are all the resources that were spent on the production and sale of products (services), they are usually expressed in value terms.

Only if you have a complete picture of the costs of producing and selling products (services) can you get a full calculation of the gross profit for the selected period.

Factors influencing gross profit

Gross profit is affected large quantity factors. They are divided into companies dependent on management and independent.

The first group of factors includes the following:

- indicator of growth in the production of goods (services) and their sales;

- improving the competitiveness and quality of goods (services) in general;

- replenishment of the range of goods (services);

- reduction in production costs;

- improving staff productivity;

- full utilization of production assets;

- systematic research of the enterprise's marketing strategies, and, if necessary, their adjustment.

Among the factors that do not depend on control are the following:

- natural, environmental, territorial, geographical conditions;

- making amendments to legislation;

- changes in state business support policy;

- transport and resource transformations in global terms.

As a result, it is necessary to have a management strategy that can be quickly adjusted, and the ability to quickly transform the policy for the production and sale of products (services).

Terms of release and sale

These actions should be aimed at maintaining the company in optimal condition. The first category of factors involves adjustment and intervention in the strategy on the part of the enterprise management. By increasing the volume of production and sales of products (services), the enterprise simultaneously increases turnover, which has a positive effect on the growth of the indicator.

An important role is given to maintaining the pace and volume of production of products (services) at fairly high positions and trying to prevent them from decreasing, as this will negatively affect the amount of gross profit.

It is important to note that finished goods inventories negatively affect the production picture, being an unprofitable load for the company. However, their implementation would help increase revenue.

Some businessmen use various methods for the most profitable sale of these unclaimed balances, and try to return at least part of the resources used for them. But these actions have a very small impact on gross profit.

Gross profit, the formula of which contains a term such as “cost”, indicates that the latter requires regular monitoring. It is important to apply innovative production technologies, search and develop more optimal options for delivering products to consumers, and look for economical energy resources and their alternative sources. These steps will help to significantly reduce costs, resulting in an increase in gross profit.

What can affect the size of the “gross profit” indicator?

The calculation formula indicates that the indicator under consideration may be influenced by the pricing policy of the enterprise. High competition forces entrepreneurs to reconsider their pricing policies. However, there is no need to strive for a constant reduction in the price of a product (service). It’s better to build a strategy to set the optimal price and stick to it, consistently making a profit, albeit a small one. In addition, it is important to regularly analyze demand in order to understand in time which product (service) it is better to refuse. After all, it is the sale of profitable products that provides the company with the opportunity to receive the maximum possible gross income, while simultaneously increasing the amount of net profit.

It is also important to monitor the level of inventory that is currently unclaimed. Storing them most likely does not pay for itself, so it is important to quickly develop measures to get rid of these stocks. Cash, obtained in this way, increase the gross profit.

Income items such as interest on deposits or shares, rental of real estate and other sources also contribute to the growth of the enterprise’s gross profit.

How to properly distribute profits

Having sold a batch of goods and received a certain amount of income, it is important to manage it wisely. This distribution might look like this:

The highest level is occupied by gross profit.

- rent;

- payment of interest on loans;

- all kinds of taxes;

- charity.

The result is net profit.

The following expense items come from net profit:

- formation social infrastructure companies and states;

- training;

- environmental funds;

- cash reserves;

- own profit of the owners of the organization.

As a result of such a distribution of gross profit, the enterprise will have the opportunity for optimal development, improvement of production, and growth of personnel potential. This will also allow you to increase your net profit in the future.

Summary

Gross profit is revenue minus cost. It differs from net profit in that it does not include variable and operating costs, as well as taxes.

Gross Profit Formula:

PV = B - C, where:

- B - revenue;

- C - cost.

To obtain the optimal gross profit, it is important to first determine the cost items that are included in the cost of goods (services), including variables that were not previously taken into account. Having an idea of all the costs of producing and selling goods (services), you can accurately calculate the amount of gross profit for a certain period.

Any commercial organization is created for the purpose of making a profit. Therefore, the determination of this indicator is one of the most important elements of analyzing the results of an enterprise. In general, profit is defined as the difference between sales revenue and costs. There are several types of profit, depending on what types of costs are included in the calculation. Let's look at how gross profit is calculated - one of the indicators most often used in analysis.

Gross profit concept

Gross profit refers to a company's profit before taxes. Those. in this case, when determining how to calculate gross profit, the calculation formula includes all costs of production and sales of products (goods, services). How to calculate gross profit in each specific case depends on the type of activity of the analyzed enterprise.

Gross profit is determined, as a rule, for a month or a multiple of a month period (quarter, half-year or year). This is due to the fact that many types of costs can only be objectively assessed based on the results of the month. Such costs include, for example, wages, taxes, rent, communal payments and so on.

But if necessary, profit can be determined at other frequencies, and also calculated for individual projects, product groups, etc.

How to calculate the gross profit of a manufacturing enterprise

For production activities, the gross profit of an enterprise is determined as the difference between sales revenue and the total cost of manufactured products.

- PR = B – SS

In this case, the cost includes all costs of production and sales of products, both direct and indirect. Cost items depend on the specifics of the activity of a particular enterprise, but the main ones can be seen when analyzing almost any production.

- Raw materials and supplies.

- Energy.

- Services of third parties (advertising, communications, audit, etc.)

- Taxes included in the cost price (on land, on property, etc.)

How to find gross profit when providing services

In this case, gross profit includes the same elements as for a manufacturing enterprise. The only difference is in the composition of the costs, taking into account which the gross profit is formed. The calculation formula will be the same as for a manufacturing enterprise, but the cost structure will be different. In this case, a significantly smaller share of costs will be made up of raw materials and energy resources, and a significantly larger share of wages.

How is gross profit determined for a trading enterprise?

For a trading enterprise, the source of profit is income from the sale of goods. Therefore, this case uses a slightly different approach to determine how to calculate gross profit. The formula will look like this:

- PR = D – SS, where:

- D – income from the sale of goods, defined as:

- D = TO – ST, where:

- TO – turnover (analogue of sales revenue for a manufacturing enterprise),

- ST – cost of purchased goods.

Cost in this case refers to the cost of selling goods. The main cost items for a trading company will be:

- Salary with deductions.

- Advertising.

- Fare.

- Costs for maintaining warehouse premises ( public utilities, security, etc.).

Sometimes, when analyzing the activities of a trading enterprise, it is more convenient to calculate profit based on turnover. In order to determine income in this case, the average trade margin is used, and then the gross profit is calculated. The formula will be like this:

- PR = (TO – TO/(1+TN)) - SS, where:

- TO – trade turnover,

- TN – average trade margin (in %).

The part of the expression enclosed in brackets is the income of the trading enterprise from the previous formula. It is defined as the difference between the proceeds from the sale of goods and the cost of their acquisition.

Example

The turnover of Alpha LLC for the reporting period amounted to 120 million rubles. excluding VAT, average trade margin - 20%, costs of selling goods - 15 million rubles. without VAT. Gross profit will be equal to:

PR = (TO – TO/(1+TN)) – СС = (120 – 120/(1 + 0.2)) – 15 = (120 – 100) – 15 = 20 – 15 = 5 million rubles.

Gross profit - formula for calculating the balance sheet

For express analysis of the results of an enterprise's activities, it is convenient to use financial statements. Its main forms are balance sheet and financial statements. financial results.

Gross profit is best determined based on the income statement data. Classic definition Gross profit in this form corresponds to profit from sales (p. 2200). To calculate it, you need to subtract the cost of sales, selling and administrative expenses from revenue.

- Page 2200 = page 2110 – page 2120 – page 2210 – page 2220

Conclusion

One of the main indicators characterizing the results of an enterprise’s activities is gross profit. This indicator is calculated based on revenue (income) and the cost of production and sales of products (goods, services). The specific calculation method depends on the direction of activity of the analyzed enterprise.

The goal of any company is to generate income. It can be calculated using different indicators. There are such concepts as revenue and net profit. Gross profit is a key indicator of a company's performance. It allows you to analyze the production efficiency of the structure.

What is gross profit?

Gross profit is the difference between income and cost. Taxes are not deducted from these funds. Cost means:

- costs of producing the product: costs of materials, equipment maintenance;

- expenses for purchasing a finished product at the purchase price;

- payment for electricity;

- salary payments.

All these indicators constitute technical costs.

IMPORTANT! VP is calculated for a specific period. The time period depends on the company. The resulting figure is indicated in the balance sheet.

What influences VP?

Gross profit changes under the influence of external circumstances, such as:

- cost of transportation services,

- natural, environmental factors,

- socio-economic environment in which the enterprise operates,

- costs of production resources,

- foreign economic contacts.

VP is also influenced by internal factors:

- income from product sales,

- other sources of income: investments, provision of services,

- cost of goods,

- demand for manufactured products, sales figures,

- cost of manufactured goods.

Gross profit is also affected by negative factors possible during the operation of the enterprise:

- overestimated or underestimated cost of products sold;

- low quality of goods;

- disciplinary violations by the company’s employees leading to losses;

- fines and sanctions.

The listed factors can affect the gross profit directly and indirectly. Factors that affect sales income have an indirect influence.

Gross profit composition

The VP may include the following financial resources:

- profit from sales of enterprise products and services;

- funds received from rural and logging farms;

- income from the sale of company property: equipment and other objects;

- amounts received from transactions not included in the main list of company activities. For example, a store sells goods. This is his main activity. However, the funds are spent on investments, the income from which is classified as non-operating profit;

- amounts received from the sale of shares.

The vast majority of EP, according to statistics, consists of income received from core activities.

Formula for calculating gross profit

Gross profit is calculated using the formula:

VP = D - (S+W)

The formula includes the following indicators:

- VP - gross profit;

- D - quantity of products sold;

- C is the cost of production of goods;

- Z - costs during production processes.

VP indicators can be calculated after the product has been produced and sold.

ATTENTION! Typically, gross profit is calculated once a year.

Example

The company produces electric kettles. Production costs are 20,000 rubles, expenses are 10,000 rubles. 500 teapots were sold per day at a cost of 1000 rubles.

Calculations are carried out as follows: revenue per day is calculated. That is, the number of teapots sold is multiplied by their cost. We will receive 500,000 rubles. From this result you need to subtract all costs, which in total amount to 30,000 rubles. From 500,000, 30,000 rubles are deducted. Gross profit will be 470,000 rubles.

Calculation features

The calculation of VP differs in a number of nuances, determined by the type of activity of the enterprise:

- If a company specializes in selling products, it is required to deduct all expenses from revenue, including discounts on goods and returns. Subtracted from the amount received. The result of the calculations is the gross profit;

- If an organization specializes in providing services, calculations are usually carried out according to a simplified scheme. Their revenues are deducted from discounts and other expenses. The resulting net profit is also gross profit.

The main stages of the calculation are standard.

Why is gross cost calculation necessary?

Gross profit does not display real income enterprises. This figure includes many unnecessary expenses: advertising, salaries, rent. VP is required for other purposes. This is a narrow, not a general tool. It is used to analyze the production resources of an enterprise. Correctly calculated indicators ensure the achievement of the following goals:

- analysis of the difference between the cost of a product and the income from its sale;

- determining the optimal cost for a product or service;

- competent measures for planning the company’s activities;

- identifying problems and weak points enterprises.

Based on the analysis of annual VP indicators, it is possible to track the economic growth of the enterprise and the results of optimizing activities.

Reflection of VP in financial statements

From financial statements It should be clear on what basis the gross profit is calculated. Let's consider the components of the calculation formula from an accounting point of view:

- “revenue” (line 2110);

- “cost price” (line 2120).

Recording of VP in documents takes into account the order of the Ministry of Finance defining accounting entries. Foreign exchange profit is indicated in line 2100.

How to increase gross profit?

Gross profit is a dynamic indicator. It constantly changes depending on the company's activities. The following activities help increase VP:

- use of LIFO technique in inventory analysis;

- tax reduction with the help of benefits that the enterprise is entitled to;

- regular write-off of bad debts from the balance sheet;

- optimization production processes, aimed at reducing costs;

- competent pricing policy that takes into account the demand for products and the general market situation;

- improving the quality of equipment to speed up the release of goods and improve their quality. Restoration or acquisition of equipment can be carried out at the expense of shareholder dividends;

- creation of reasonable standards to ensure control over intangible assets.

IMPORTANT! Gross profit is an indicator on the basis of which planning of an enterprise’s activities in the production sector can be carried out.

So.

Gross profit is the amount obtained after deducting costs and production costs. Determined by formula. The nuances of the calculation depend on the type of activity of the enterprise. The VP indicator is important for assessing the company's production resources. Is the basis for reasonable pricing. Gross profit is reflected in the financial statements using the appropriate entries established by the Order of the Ministry of Finance.

Gross profit is one of the key indicators of the financial performance of an enterprise. Below you will find a definition of the term, a formula for calculating gross profit and a description of the meaning of the indicator.

What is gross profit

Gross profit is the company's revenue minus the cost of the product. If a pottery workshop sold 10 pots worth 10,000 rubles in a week, to calculate the gross profit you need to know the cost of their production.

It includes the cost of clay, water, electricity, and wages for the craftsman. Expenses should also include depreciation of the potter's wheel and the cost of renting the premises. If the pots were sold through a nearby store, the cost should include the costs of transporting the products and the distribution network’s commission.

If the amount of expenses is 6,500 rubles, and the revenue is 10,000 rubles, then the gross profit of the workshop is 3,500 rubles.

Formula for calculating gross profit

Gross profit is calculated using the following formula:

Vyr – C = PRval

The variables are deciphered as follows: Vyr - revenue, C - cost, PRval - gross profit.

This is the classic formula used by manufacturing companies. Merchants calculate gross profit using the gross revenue variable:

Inhalation – C = PRval

Traders operate with the “gross income” variable, since they redistribute a significant part of the proceeds in favor of producers. For example, in order to sell a ton of apples for 10 thousand rubles, a retail chain must buy this product from the manufacturer for 8 thousand rubles. After the sale, the merchant’s revenue will be 10,000 rubles, and the gross income will be 2,000 rubles.

What is the meaning of the “gross profit” indicator?

Gross profit is one of the key performance metrics manufacturing enterprises. It shows how effective business processes are in general and the production activities of the organization in particular.

A simplified example of a pottery workshop shows that its activities are effective. The cost of manufactured products was 6,500 rubles. And the proceeds from the sale of pots amounted to 10,000 rubles. At the same time, the cost included all expenses for production activities, including depreciation of equipment.

Despite the positive gross profit, the activities of a hypothetical pottery enterprise may be unprofitable. This will happen if the amount of taxes and fines exceeds 3,500 rubles or the amount of gross profit. In this case, the net profit will be negative.

To increase gross profit, a company can reduce the cost of production or increase its cost to consumers. The second way reduces the competitiveness of the organization, so it should be used only after all possibilities for reducing production costs have been exhausted. Specific steps depend on the industry, economic situation and a variety of other factors. Some of the most obvious ways to reduce product costs include:

Reducing labor costs. In this case, you will have to increase the workload on existing specialists, but not hire new ones.

Reducing the cost of raw materials.

Scaling production.

Energy saving.

Reduced logistics costs.

Reducing costs for selling products.

Improving marketing efficiency.

Trading enterprises practically do not use gross profit to evaluate performance. Enterprises of this type focus on profitability and sales volume, net profit and other indicators.

So, gross profit is an indicator of the financial performance of an enterprise. It is calculated as the difference between revenue and production costs. Gross profit is convenient to use to evaluate the performance of manufacturing enterprises.